The federal government’s Old-Age, Survivors, and Disability Insurance (OASDI), better known as Social Security, was established in 1935 by President Franklin D. Roosevelt during the depths of the Great Depression. Its purpose was to provide financial assistance to older Americans and others facing economic hardship due to age, disability, or the loss of income. Designed as a social safety net, Social Security provides monthly benefits intended to replace a portion of a worker’s pre-retirement earnings and help retirees maintain a basic level of financial security.

When it was first launched, many viewed the program as a temporary response to an unprecedented economic crisis and believed it would remain fully self-funded. More than 90 years later, neither assumption has proven true.

The Headlines are Hard to Ignore

The recent release of “The 2026 OASDI Report” has triggered widespread retirement worries and an onslaught of media headlines that present a dire picture of America’s Social Security’s program. According to several financial news outlets, the trust fund is headed toward funding shortfalls, deep benefit cuts, and even complete collapse.

The recent release of “The 2026 OASDI Report” has triggered widespread retirement worries and an onslaught of media headlines that present a dire picture of America’s Social Security’s program. According to several financial news outlets, the trust fund is headed toward funding shortfalls, deep benefit cuts, and even complete collapse.

The panic is coming from a bulleted highlight from this year’s report under the heading “Trust Fund Reserves and Reserve Depletion.”

“The OASI Trust Fund is projected to become depleted in the fourth quarter of 2032, one quarter earlier than projected in last year’s report. Upon reserve depletion in 2032, projected income is sufficient to pay 78 percent of scheduled benefits. This percentage declines gradually to 62 percent by 2100.”[1]

There’s no doubt that Social Security is experiencing a funding crisis which has pundits and experts alike sounding the alarm on the program’s viability.

This is not a small concern. Over 70 million Americans currently receive monthly Social Security payments. A staggering 1 in 5 Americans collect regular benefits including retirees, disabled workers, and survivors of deceased workers. For many, it is now the only retirement plan and economic support they have. According to a Public Benefits expert at Rutgers Law School if Congress does not act, cuts are imminent.

“In the absence of Congressional action in the next six years to solidify trust fund financing, social security recipients will suffer automatic 20-24% across-the-board reductions in benefits … More than half (52-56%) of social security beneficiaries derive 50% or more of their total income from social security and approximately a quarter (24-27%) garner 90% or more from these benefits. A 20-24% cut would be quite significant for most and devastating for at least a quarter of all recipients.”[2]

Popular, Expensive, and Unsustainable

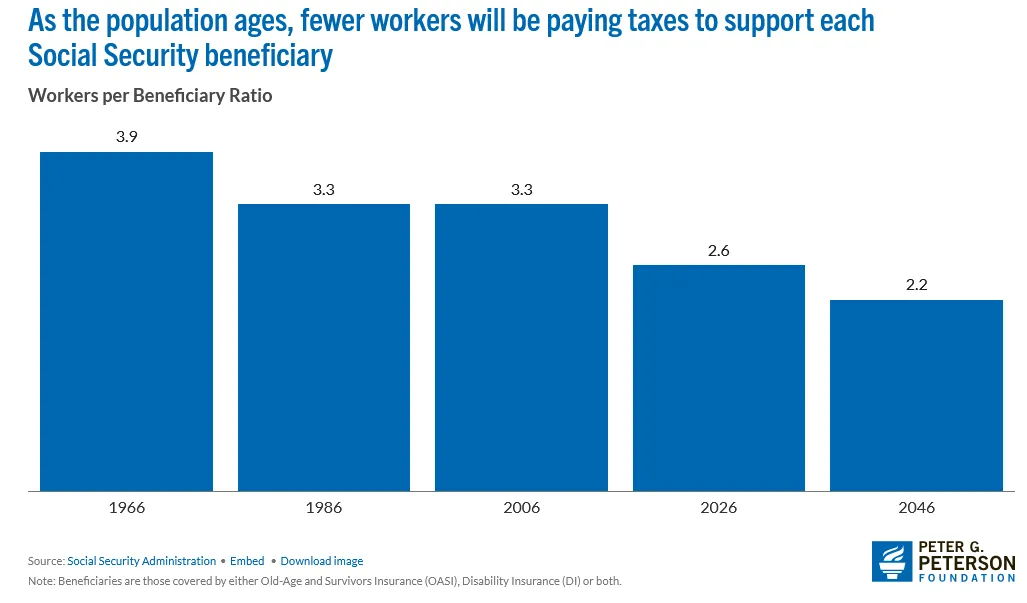

Social Security’s financial outlook has worsened for an array of reasons and none have an easy solution. From an aging population, to fewer workers contributing, to rising costs … the entire system is under pressure.

“As a result of the nation’s changing demographics, the number of workers contributing to the program is growing more slowly than the number of beneficiaries receiving monthly payments. In 1966, there were 3.9 workers per beneficiary; that ratio has dropped to 2.6 today and will continue to fall in the future.”[3]

Social Security is the single largest line item in the federal budget. Last year the U.S. government spent 22.5% of all public funds on the program or $1.58 trillion. Almost 90% of people aged 65 and over are enrolled in Social Security[4]. And with almost 11,000 Americans turning 65 every day, sustainability comes into question.

The program’s solvency isn’t just a math problem; however, it’s a widening gap between revenue, benefits, and costs. And the greatest challenge isn’t actually financial; it’s political. While reform is widely viewed as necessary, any lawmaker who proposes meaningful changes risks touching the “third rail” of American politics and paying a harsh political price.

A senior fellow at the American Enterprise Institute has outlined several proposals to strengthen Social Security’s finances. While practical on paper, many would not only be unsettling to current and future retirees but extremely unpopular politically.

- Social Security currently pays extra benefits to millions of retired spouses, increasing their monthly benefits by nearly 50%. These beneficiaries did not pay for these additional benefits, and many don’t need them.

- Congress might consider raising Social Security’s early retirement age of 62, which would have little effect on Social Security finances but which the Congressional Budget Office estimates would increase gross domestic product by about one percent.

- Large benefit cuts for the rich could be coupled with expanding Supplemental Security Income (SSI) for the poor, creating a strong but affordable guarantee against poverty in old age.

- The federal tax preference for retirement savings appears to do little to increase savings, while costing the federal budget 1.3% of GDP annually.[5]

“It Won’t Be There for Me!”

For decades, Americans have worried that Social Security won’t be there when they need it. Younger workers question whether they’ll ever be able to collect on the benefits they’ve paid in, while current retirees worry that their payments and benefits will be dramatically reduced. These concerns are no longer far-fetched but supported by the program’s own projections.

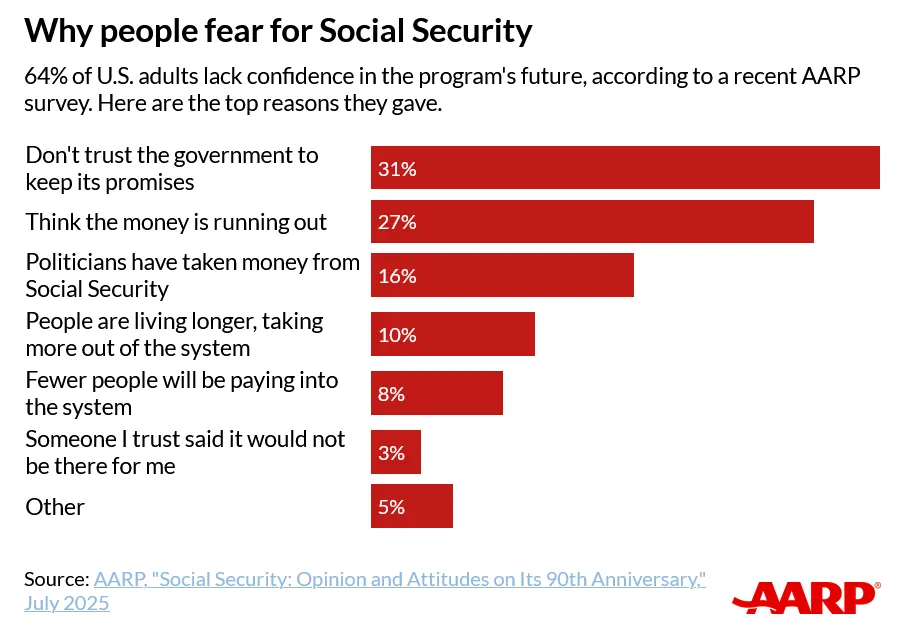

Suffice to say, confidence in the program has dipped dramatically. Americans have lost trust in the government and the politicians to shore it up and question the viability of the structure itself to provide the financial safety and security that it was designed to deliver.

Suffice to say, confidence in the program has dipped dramatically. Americans have lost trust in the government and the politicians to shore it up and question the viability of the structure itself to provide the financial safety and security that it was designed to deliver.

According to a recent survey by AARP, only 36% of respondents felt confident about the program’s future with the majority citing a lack of trust in government and available funds simply running out as their primary worries.[6]

Non-partisan think tank, Brookings Institution, believes Social Security faces imminent insolvency and the push for program reform is actually moving backwards. The research group suggests that it may take a painful crisis to finally compel change.

“Not only have policymakers largely failed to engage with the problem, Congress and the president have recently enacted laws and pursued policies that worsen the program’s financial status. Absent imminent crisis, recent presidents and lawmakers have had little incentive to address Social Security’s long-term fiscal deficit. With insolvency looming, policymakers might actually welcome a crisis to force their hands to forge a fix for Social Security.”[7]

Planning Has Never Been More Important

The 2026 OASDI Trustees Report makes one thing clear … Social Security was never intended to be an all-encompassing retirement plan. As the program faces mounting financial pressure, relying on it as a primary source of retirement income increases your level of risk.

While Congress may ultimately be forced to act to save the program, the timing and trade-offs are unknown. And this is precisely why many experts urge retirees and pre-retirees to diversify their assets. Physical gold has become an important part of that strategy.

While Congress may ultimately be forced to act to save the program, the timing and trade-offs are unknown. And this is precisely why many experts urge retirees and pre-retirees to diversify their assets. Physical gold has become an important part of that strategy.

Unlike government promises or paper assets, gold is tangible, has no counterparty risk and has a long history of preserving purchasing power during periods of economic uncertainty, fiscal instability, and political paralysis.

While no one can predict whether Social Security will survive or how or when program reform will occur, taking immediate steps to diversify and protect your retirement savings may prove far more valuable than waiting for Washington to act.

ORION METAL EXCHANGE is a Leading Precious Metals Dealer

With Live Pricing, Low Commissions and Top-Rated CUSTOMER SERVICE.

Call Now for a FREE Investor Kit!

REPRESENTATIVES ARE AVAILABLE NOW AT: 1-800-559-0088

1 https://www.ssa.gov/oact/TR/2026/tr2026.pdf

2 https://law.rutgers.edu/news/social-security-funding-crisis

3 https://www.pgpf.org/article/social-security-will-be-depleted-by-2032-and-other-takeaways-from-the-trustees-report

4 https://usafacts.org/articles/how-much-does-the-us-spend-on-social-security-is-it-sustainable/

5 https://www.aei.org/articles/social-security-reform-the-math-is-easy-the-politics-are-hard-and-this-is-the-wrong-way-to-look-at-it

6 https://www.aarp.org/social-security/ssa-trust-confidence

7 https://www.brookings.edu/articles/moving-backwards-on-social-security-reform