When we think about retirement, we envision rest, relaxation, freedom, and new beginnings. Mornings without alarm clocks, afternoons without deadlines, and weeks without the pressures of the daily grind seem like well-earned rewards for a lifetime of hard work. But then along comes economic reality.

Today’s retirees face an increasingly uncertain financial future. Inflation steadily erodes the purchasing power of retirement savings, while market volatility puts nest eggs at risk, particularly for those heavily invested in equities. And no matter how much we’ve saved, many retirees still wonder whether their money will last as long as they do.

The first step toward achieving peace of mind in retirement is understanding and preparing for the financial risks that can threaten it.

Inflation and the Loss of Purchasing Power

Inflation has been called many things by many people. Milton Friedman called it taxation without legislation. John Maynard Keynes believed it was a means for government to confiscate wealth. And Ronald Reagan portrayed it as an armed robber, mugger and hit man.

According to a recent article in Forbes, it is all of these things.

According to a recent article in Forbes, it is all of these things.

“Inflation is an important and often overlooked factor in retirement planning because it affects purchasing power, investment performance, and long-term financial security. Over time, inflation increases the cost of everyday expenses such as housing, healthcare, food, transportation, and utilities … This can create serious challenges for retirees because fixed incomes and conservative investments may fail to keep pace with rising costs. Everyday necessities quickly become more expensive, and healthcare costs, which already tend to rise faster than average inflation, can place additional pressure on retirement savings.”[1]

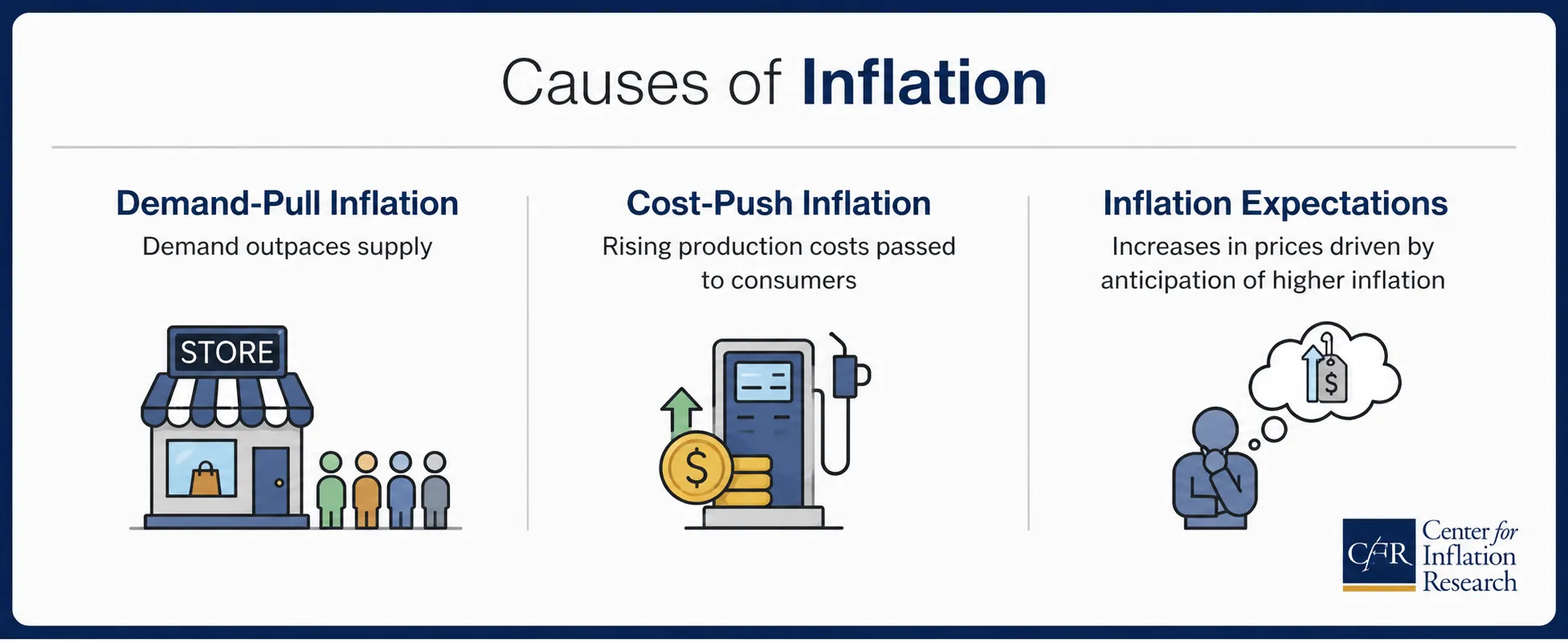

Inflation is caused by a combination of factors including demand spikes, supply chain challenges, rising production costs, and monetary policy. The Federal Reserve Bank of Cleveland categorizes inflation triggers this way:

- Inflation can increase when growing demand outstrips changes in the supply of goods and services. Economists call this “demand-pull inflation.”

- Another source of higher inflation is known as “cost-push inflation,” which occurs when the cost of producing these goods and services rises notably or when they can’t be produced to meet demand.

- Inflation can also rise on people’s expectations about where it will be in the future. These expectations influence economic decisions, and this, in turn, affects inflation.[2]

While inflation has many causes, its impact on retirees is undeniable. It drives up the cost of everyday necessities … from groceries, to gas, to healthcare … and reduces the purchasing power of the dollar. And for those living on a fixed income, that means depleting savings, pensions, and IRA accounts more quickly than anticipated just to cover essential expenses.

Market Volatility and Portfolio Risk

Another threat to retirement accounts is turbulence on Wall Street. Large swings in stocks and bonds can not only cause portfolio losses but also destroy long-term wealth. Wars, terror attacks, trade disputes, pandemics, recessions … Wall Street often reacts on a hair trigger and the ups and downs of market volatility can take a financial toll on those living off of their accumulated savings.

“Uncertainty in the market impacts retirement planning in several ways. It can cause a significant decline in investment portfolios, meaning retirees relying on their investments may face reduced savings. Market downturns also diminish the returns on investments, potentially jeopardizing long-term goals.”[3]

Pullbacks and corrections are a normal feature of investing and attempting to time, wait out, or predict the markets is not only difficult but could prove costly as panic and selloffs often result in further losses.

Charles Schwab looked at 50 years of S&P 500 data from 1975 through 2025 and found that market declines and bear markets are actually the “norm” and not the “exception”:

- The average maximum drawdown in a calendar year is about 15%. That means investors can expect a decline of roughly 15% from peak to trough in a typical year.

- Maximum drawdowns reached 20% or more in 14 of those years — nearly one of every three years. It exceeded 30% five times or about once every 10 years.

- Some drawdowns stretched across multiple calendar years. Looking at rolling two-calendar-year periods, we found that the biggest drawdown exceeded 20% in half of them.

- The maximum drawdown exceeded 30% in 21 of the 50 five-year rolling periods.[4]

Needless to say, data like this demonstrates the very real impact of market volatility on the value of stocks held in a 401k, IRA or pension plan and the persistent threat to retirement dollars. It also underscores the importance of portfolio diversification and holding assets that behave differently than traditional investment vehicles.

A Fate Worse than Death?

If chronic inflation and market volatility aren’t enough to keep retirees up at night, one fear looms even larger: running out of money.

If chronic inflation and market volatility aren’t enough to keep retirees up at night, one fear looms even larger: running out of money.

According to the Allianz Center for the Future of Retirement, older Americans fear outliving their money more than death:

- 67% worry more about running out of money than dying

- 48% do not have a written financial plan

- 57% feel anxious about their future financial well-being when retirement accounts decline during a market drop[5]

Americans are living longer, so retirement is lasting longer too. With the average U.S. retirement age around 63, men may need to fund roughly 13 years of retirement, while women may need to fund nearly 18 … relying heavily on savings, pensions, Social Security, and investment income.

And as we age, healthcare costs loom increasingly large and may become one of the greatest threats to retirement income according to a new report from the Life Insurance Marketing and Research Association (LIMRA).

- More than three-quarters of U.S. adults live with at least one chronic illness, and over half have multiple chronic conditions.

- Roughly 40% of Americans will develop cancer during their lifetime, with diagnosis most common around retirement age.

- Cardiovascular disease affects more than half of adults over age 40 and remains the leading cause of death in the United States.

- As life expectancy increases, many Americans experience a growing gap between lifespan and healthspan, spending up to 10–12 years managing chronic illness or disability later in life.[6]

We will obviously never eliminate uncertainty at any stage in life, particularly when it comes to retirement dollars versus retirement costs. We also cannot predict the future, but we can make informed decisions based upon facts and data. So, for retirees and pre-retirees, a diversified retirement strategy can help navigate the perils of economic peaks and troughs … as well as market boom and busts.

We will obviously never eliminate uncertainty at any stage in life, particularly when it comes to retirement dollars versus retirement costs. We also cannot predict the future, but we can make informed decisions based upon facts and data. So, for retirees and pre-retirees, a diversified retirement strategy can help navigate the perils of economic peaks and troughs … as well as market boom and busts.

The bottom line is preparation brings peace of mind. And while no investment can eliminate risk, precious metals have long served as an inflation hedge, a store of value, and a natural portfolio diversifier. For many retirees, gold can play an important role in preserving purchasing power and strengthening long-term financial security. After all, there’s a reason they’re called the “Golden Years.”

ORION METAL EXCHANGE is a Leading Precious Metals Dealer

With Live Pricing, Low Commissions and Top-Rated CUSTOMER SERVICE.

Call Now for a FREE Investor Kit!

REPRESENTATIVES ARE AVAILABLE NOW AT: 1-800-559-0088

1 https://www.forbes.com/sites/davidkudla/2026/05/28/why-inflation-may-be-the-biggest-threat-to-your-retirement/

2 https://www.clevelandfed.org/center-for-inflation-research/inflation-explained-your-guide-to-inflation-basics/what-causes-inflation

3 https://www.myubiquity.com/resources/the-impact-of-market-volatility-on-retirement-planning

4 https://www.schwab.com/learn/story/ups-and-downs-stock-market-volatility

5 https://www.usatoday.com/story/money/2026/05/04/retirement-fears-outliving-savings/89897704007/

6 https://www.limra.com/en/newsroom/news-releases/2026/health-related-costs-are-the-greatest-threat-to-retirement-security-new-research-finds/