Deutsche Bank, one of the world’s largest financial institutions, has issued a bullish outlook for gold over the next few years. What’s most noteworthy, however is that the bank’s price prediction isn’t driven by traditional catalysts like inflation or market volatility, rather it’s rooted in something far bigger … the accelerating shift toward de-dollarization especially across developing economies.

The investment bank’s foreign exchange models project a steady rise in gold’s share of global reserves particularly among central banks in emerging markets which could potentially drive gold prices up more than 75%. The research note from Germany’s largest bank is garnering a lot of attention and gaining traction among investors focused on long-term wealth protection, as it points to a structural shift in the global gold market.

The De-Dollarization Effect

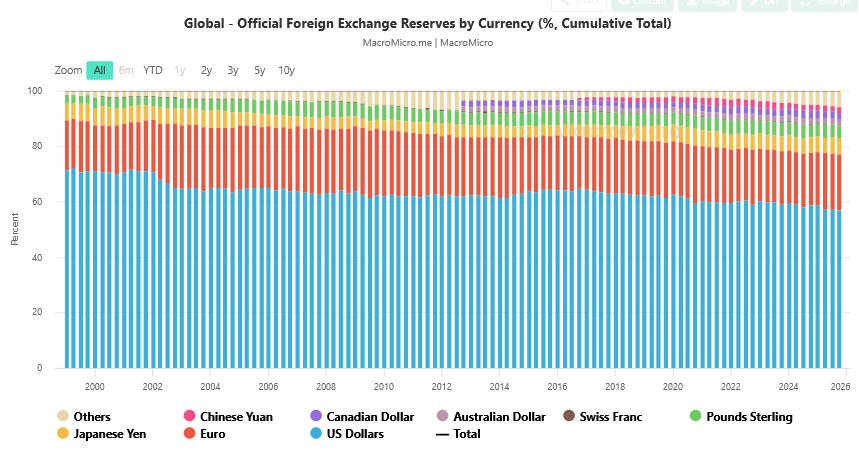

The term “de-dollarization” references the steady decline in reliance on the U.S. dollar in international trade and global transactions. Note in the chart to the left from Mico Macro, in Q1 of 1999, the U.S. dollar was over 71% of foreign exchange reserves. In Q4 of 2025, it dropped to under 57%. [1]

According to JP Morgan, the decreasing demand for the greenback points to a structural shift that is linked to the erosion of American exceptionalism as well as the rise in the credibility of other currencies which could undermine dollar-held investments.

“Fundamentally, de-dollarization could shift the balance of power among countries, and this could, in turn, reshape the global economy and markets. The impact would be most acutely felt in the U.S., where de-dollarization would likely lead to a broad depreciation and underperformance of U.S. financial assets versus the rest of the world.” [2]

It’s also important not to underestimate the politics of de-dollarization. The dollar has long been weaponized, from asset seizures and SWIFT exclusions, to sweeping economic sanctions … giving America a powerful tool to punish or isolate its adversaries.

According to financial learning platform, Analyst Prep, Russia’s 2022 invasion of Ukraine and the subsequent freezing of billions of dollars in Russian assets, was a de-dollarization rallying cry that translated to the notion of ‘play nice in the global sandbox, or your greenbacks will be seized.’

“The ability to cut a country off from the dollar system is a powerful tool. It has pushed nations to create their own payment systems and settle more trade in local currencies. For them, this is about financial sovereignty; having control over their own money … Consequently, countries like China, India and others started thinking hard about how to protect themselves.” [3]

A Broad, Global Shift Toward Gold Reserves

The central banks of China and India are among the biggest gold buyers of the past decade along with Poland, Turkey and Russia. In the last five years, the world’s leading monetary authorities net-purchased 463 tons of gold, bouncing back from lower buy-rates in 2020 primarily due to the economic impact of Covid-19.

According to the World Gold Council (WGC), in 2026 there continues to be persistent demand for gold from central banks amid rising geopolitical tensions and ongoing inflation pressures:

“Central bank gold demand began 2026 strongly, with estimated net purchases of 244t in Q1. Demand exceeded both the previous quarter and the five-year average, underscoring continued commitment to strengthening reserves with gold. During the quarter, central banks had to contend with heightened uncertainty on multiple fronts. The conflict involving Iran, the US and Israel added to an already fraught geoeconomic environment, driving greater volatility across markets including gold.” [4]

WGC data ranks the National Bank of Poland as the largest purchaser of gold in Q1 of this year, increasing its gold reserves by 31t. The Central Bank of Uzbekistan added 25t to its reserves, while the People’s Bank of China increased its gold reserves by 7t.

Other buyers include a host of developing nations:

- National Bank of Kazakhstan (12t)

- Czech National Bank (5t)

- Bank Negara Malaysia (5t)

- Bank of Guatemala (2t)

- National Bank of Cambodia (2t)

- Bank Indonesia (2t)

- National Bank of Serbia (1t)

- Central Bank of the UAE (1t)

The uptick in gold buying by emerging economies, reflects a strategic shift in how low-to-middle income countries are managing their reserves. Rather than rely on U.S. dollar–denominated assets, these nations are increasing allocations to gold as a neutral store of value. The precious metal not only acts as a critical counter-balance to inflation, currency instability, and rising geopolitical tensions, but also provides greater financial independence and security.

“Unimpeachable Global Collateral”

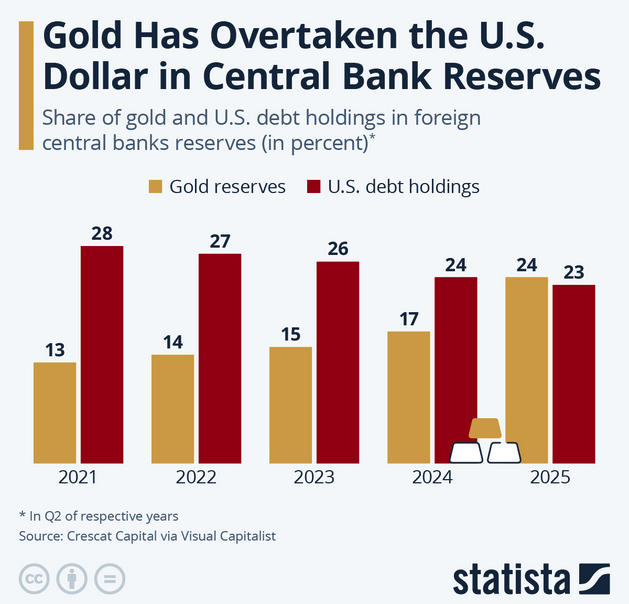

The massive surge in central bank gold acquisitions and the sustained buying trajectory is a classic example of rising demand meeting limited supply. And for the first time in 30 years, gold has officially overtaken the dollar as the world’s largest global reserve asset.

The massive surge in central bank gold acquisitions and the sustained buying trajectory is a classic example of rising demand meeting limited supply. And for the first time in 30 years, gold has officially overtaken the dollar as the world’s largest global reserve asset.

“Dollar-denominated reserves – i.e. central bank holdings – adjusted for valuation effects are now lower than gold reserves for the first time since the International Monetary Fund started publishing the data in the late 1990s … The market has re-alighted on the age-old solution of gold as unimpeachable global collateral — to the detriment of the US currency — after growing distrust in the dollar standard and a lack of viable alternatives to assets separate from the financial system.” [5]

Gold is now the beneficiary of an increasingly divided world replete with trade wars, regional disputes, sanctions, capital controls, and financial embargoes.

This shifting environment is one reason that Deutsche Bank believes central banks, particularly in emerging economies, will continue to aggressively accumulate gold in the years ahead.

“The German investment bank said it sees a scenario where central banks, especially those in emerging economies, continue to increase their gold holdings as a financial safety net to protect themselves from Western sanctions. The bank highlights that these central banks have added over 225 million ounces to their reserves since the 2008 financial crisis, while their holdings of US dollars have fallen from a peak of over 60% in the early 2000s to about 40% today.” [6]

According to the bank’s reserve-allocation model, gold’s share of global central bank reserves could rise from roughly 30% today to 40% in the years ahead. Bank analysts believe that shift could support gold prices exceeding $8,000 per ounce.

As gold continues evolving from an “alternative asset” into a “strategic reserve asset,” the metal will likely undergo significant long-term repricing. Unfortunately, many investors only react after major price moves are already underway.

The question is whether you will position your portfolio to benefit from that price shift or merely chase after it later.

ORION METAL EXCHANGE is a top-rated

GOLD IRA DEALER with Best-in-Class CUSTOMER SERVICE.

Call for a FREE Investor Kit and up to $30K in FREE metals (on qualifying purchases).

REPRESENTATIVES ARE AVAILABLE NOW AT: 1-800-559-0088

1 https://en.macromicro.me/charts/116488/global-official-foreign-exchange-reserves-by-currency-share

2 https://www.jpmorgan.com/insights/global-research/currencies/de-dollarization

3 https://analystprep.com/blog/de-dollarization-us-dollar-dominance/

4 https://www.gold.org/goldhub/research/gold-demand-trends/gold-demand-trends-q1-2026/central-banks

5 https://www.bloomberg.com/news/articles/2026-04-09/war-has-caused-lasting-damage-to-the-dollar-system-macroscope-mnrlrgh4

6 https://www.mining.com/gold-price-could-see-8000-on-de-dollarization-deutsche-bank-projects/